Cycle Accruals [U0301]

'B' Method IBLs: refer to the

Interest Accrual After Maturity section of the Interest Bearing Loans overview document for more information on how LeasePak accrues interest on loans after maturity.

'B' Method IBLs: refer to the

Interest Accrual After Maturity section of the Interest Bearing Loans overview document for more information on how LeasePak accrues interest on loans after maturity.

Introduction

The Cycle Accruals update [U0301] is used to accrue or reverse accruals interactively for a lease. There is also the option to accrue for a selection of leases or for all leases in the entire LeasePak system. All leases selected are accrued to their current point, as determined by the system based on the current date. "Catch-up" accruals are performed if the lease has missed more than one accrual. Selected leases that are already current are not accrued. Therefore, a lease is never accrued past its current point, regardless of the number of times the Accrual option is selected for the lease.

The Cycle Accruals update is normally automatically run during the End of Period process [U04] according to predefined cycles. These cycles are specified through the Predefined Cycles Customizations option of the Portfolio update [U0212].

Cycle Accruals may also be performed interactively, without affecting the normal End of Period operation (if the leases are already accrued from the interactive update, the Exception report will list them as such). The update can be accessed through the LeasePak Update menu, Predefined Cycle option or by entering U0301 into the Fast Menu <F2>.

Cycle Accrual processing can not be applied to leases in non-accrual status.

The accrual process performs the following functions:

- Income

Recognition

Income is recognized for the lessor, vendor, investor, IDC/IDR and ITC for book purposes according to the specified accrual method(s). If a lease is in a suspended earnings status, income and receivables accrued are placed in the suspended General Ledger accounts. The amount of income accrued is accumulated in a field on the Master Financial (RLS) file, for later use if earnings are reinstated for the lease.

- Accounts Receivable

- Accounts receivable for lease payments is established if a payment is due.

- Use Tax Calculation and Accrual

Use tax is calculated and added to the accounts receivable. If there are multiple assets for the lease, the use tax for each asset is calculated separately based on the location of the asset, the appropriate tax rate for the location, and any use tax ceilings that may be in effect for the particular taxing entity. (A use tax ceiling is a maximum use tax amount per payment established by the taxing entity.)Use tax is calculated based upon the current tax payment code and location of the asset. Incorrect use tax may be calculated if the location and/ or tax payment code is changed during the period for which the accrual process is performed.

The Accounts Receivable (RAR) file contains fields which make it possible to prorate sales tax for partial payments. These fields (PRIN_STAX_C and INT_STAX_C) are automatically set to Y if sales tax is due for an item. If a partial payment of a taxable item is received, LeasePak calculates the portion of the payment which should be applied to sales tax. Thus sales tax receipts correspond closely to taxable gross receipts.

LeasePak may cause a $0.01 difference for IDC/IDR's on some IBL's when an accrual, accrual reversal and a re-accrual is performed.

LeasePak may cause a $0.01 difference for IDC/IDR's when the amortized IDC/IDR is reversed.

LeasePak always uses the tax rate applicable to the lease due date, not the tax rate applicable to the date on which the accrual occurred

Note: LeasePak maintains accrual, accrual reversal & accrual revesal (suspended) general ledger entries to amortize dealer bonus. To amortize the dealer bonus amounts LeasePak works same as is it does today for IDC3, Fixed Rate Reserve.

NOTE: LeasePak produces the following accrual general ledger entries to amortize dealer reserve. To amortize the dealer reserve amount LeasePak will work same as it does today for IDC3, Fixed Rate Reserve.

Alternate Accrual/Billing Cycles: For details of supported accrual methods for use with non-monthly accrual/billing cycle leases, refer to Alternate Accrual/Billing Cycles overview document.

Four reports are produced by the Accrual option of the Cycle Accruals update [U0301]:

- Precomputed

Income Accrual Register

All leases accrued with a precomputed income method (FASB level yield, Rule of 12/78ths, Rule of 12/78ths Half Month Convention, and straight line) are displayed on this report. Precomputed income accrual methods are characterized by the use of contract receivable and unearned income General Ledger accounts. The total amount of income to be earned over the term of the lease can always be determined at commencement.

The following table explains how earned income will be calculated for different accrual methods:

Accrual Method Accrual/Billing Cycle Income AAPR, RAPR Bi-Weekly Earned income = Net Investment * Yield / 26 Monthly Earned income = Net Investment * Yield / 12 Semi-Monthly Earned income = Net Investment * Yield / 24 Weekly Earned income = Net Investment * Yield / 52 AOSL, ROSL Bi-Weekly Operating Income = Total Payments / Term (Months) / 12 *26 Monthly Operating Income = Total Payments / Term (Months) Semi-Monthly Operating Income = Total Payments / Term (Months) * 2 Weekly Operating Income = Total Payments / Term (Months) / 12 * 52

- Simple

Interest Accrual Register

All leases accrued with a simple interest income method, fixed or floating, are displayed on this report.

- Operating

Lease Accrual Register

All operating leases are displayed on this report. Operating leases recognize the entire lease payment as income. Straight-line operating leases recognize an average monthly payment as income. The difference from the actual amount due is recorded as unbilled income.

- Accrual

Message Report

This report contains exception information for special messages and errors encountered during the accrual process. It should always be reviewed after any accrual process.

The Accrual Reversal option of the Cycle Accruals update [U0301] reverses the accrual process for a specific lease. For example, one use of the Accrual Reversal option occurs when adding an asset to a lease as of a past date. In this process, the accruals for the lease are reversed to the date the asset is to be added, then the asset is added using the Asset Add-on update [U0113], and the lease is re-accrued using the Accrual option of the Cycle Accrual update [U0301].

Another example of the use of the Accrual Reversal option is payment reschedule for a lease as of a past date. In this process, accruals for the lease are reversed to the date of the payment reschedule, then the payments are rescheduled using the Payment Reschedule update [U0104], and the lease is re-accrued using the Accrual option of the Cycle Accrual update [U0301].

No reports are produced by the Accrual Reversal option of the Cycle Accruals update [U0301].

Use tax is calculated based upon the current tax payment code and/or location of the asset. Incorrect use tax may be calculated if the location and/or tax payment code is changed during the period for which the accrual reversal process is performed.

If a previous payment schedule adjustment has been done, such as through the Asset Payoff/Termination options of the Payoff update [U0103], the Payment Reschedule update [U0104], or the Asset Add-on update [U0113], and accruals are reversed to before the date of the schedule change, incorrect income may be reversed.

LeasePak will allow for Multiple Due Day changes to be made to a lease via the Payment Due Day Change [U0118] update when the MULTI DUE DAY CHANGE RESTRICTION field is set to 'Y'. Every time the Due Date is changed, the final payment day will change, based on certain lease criteria. There will be no restriction on the number of times the Due Date can be changed throughout the life of the lease. An edit check will be in place so as to not allow a Due Date Change for more than 25 days per occurrence.

Also, the entire amount of recurring charges on the invoice(s) to reverse is waived. This includes any recurring charge amounts which may have been manually assessed.

LeasePak allows a user to create an advanced invoice, and checks for an advanced invoice that already exists and add to that invoice if it exists.

When accruing an invoice that already exists an advanced invoice, LeasePak checks for any lease-level assessments that have been added and include

them in the accrual by making the appropriate GL's and all updates that would be made through U0105 when assessed on accrued invoice, except increasing

the manual assessment bucket on lease.

Running cycle accruals and an advanced invoice is to be created; LeasePak checks to see if an invoice is already exist for that due date. Because

of the change where assessments can be placed on advanced invoice, and advanced invoice with only assessments on it can exists.

Performing accruals on an advanced invoice, LeasePak checks at the lease's payment schedule and recreates the invoice with the amount on the

payment schedule. Checking payment schedule is important because the payment schedule may have been changed since the advanced invoice was

created and the advanced invoice will not have changed to match the new payment schedule. It will also recalculate the sales tax in case

the rates have changed. After recalculation, LeasePak cannot delete the advanced invoice and recreate it with the new payment schedule.

The accrual process also includes additional assessments that have added and use the recurring charge amount on the advanced invoice instead

of the recurring charge amount on the recurring charge payment schedule.

The accrual reversal process checks advanced invoices for additional assessments and leave them on the advanced invoice if they exist when

reversing the other amounts.

Note: Once accrual reversal is done any changes to, the recurring charges on an invoice will be lost. When the invoice is re-accrued, the recurring charge will be reset to the amount on the recurring charge payment schedule. This is different from assessments on invoices, which will not be reversed during an accrual reversal, but will remain on the invoice and therefore no changes to them lost.

For Vertex O users only: To process cycle accruals and calculate tax for Vertex O lease using Vertex O interface. LeasePak uses Vertex O interface to send taxable information to the Vertex O server and Vertex O server returns the calculated tax. Following exceptions may occur while processing accruals for vertex O leases:

For Vertex O users only: To process cycle accruals and calculate tax for Vertex O lease using Vertex O interface. LeasePak uses Vertex O interface to send taxable information to the Vertex O server and Vertex O server returns the calculated tax. Following exceptions may occur while processing accruals for vertex O leases:

- ERROR ENCOUNTERED MISSING ASSET TAX AREA ID

All assets on a lease being accrued using Vertex O must have tax area IDs for the equipment location in order to calculate tax. - ERROR ENCOUNTERED MISSING VENDOR TAX AREA ID

All leases being accrued using Vertex O must have a lease level vendor with a tax area ID on the vendor address.

- ERROR VERTEX O SERVER NOT RESPONDING

when attempting to calculate tax using Vertex O, the Vertex server did not respond.

Accrual Cycle

The accrual cycle serves 2 functions:

- defines the day(s) of the month on which a payment may be due

- determines when it is time to run the Cycle Accrual from the End of Period function [U04]

All possible payment due days are established in the accrual cycle through the Predefined Cycles Customizations option of the Portfolio update [U0212]. Lease payments may be due only on a valid payment due day. Payment due days also trigger the accrual process during the End of Period process [U04].

Accrual Day

The date on which any particular lease is accrued is based on 3 factors:

- the payment due day of the lease

- the accrual cycle established through the Predefined Cycles Customizations option of the Portfolio update [U0212]

- the accrual deferral days for the portfolio (established through the Miscellaneous Customizations option of the Portfolio update [U0212])

Late charge grace days at the lease level (established through the Book Lease option of the New Lease update [U0101]) is not used in accrual cycle calculations. It is used in late charge calculations only.

To determine the day on which a lease accrues:

- Add the portfolio accrual deferral days to the payment due day of the lease.

- If the resulting number is greater than 31, subtract 31 from the number.

- The first day in the accrual cycle on or after this day is the day the lease is accrued.

For example, assume that the accrual cycle is set up for the first, fifth, tenth, fifteenth, twentieth and twenty-fifth days of the month. A lease billed in advance with a payment due date of February 10 will accrue income for the February 10 payment on January 10 with an accrual deferral period of zero days, January 15 with an accrual deferral period of 5 days, or January 20 with an accrual deferral period of 10 days.

LT method leases do not accrue until the due day of the payment plus grace days has past.

With the 1994 JULE Fund the first accrual period may be longer than subsequent accrual periods for level yield leases billed monthly in arrears and for fixed rate IBLs using the principal and interest accrual method billed in arrears. This is accomplished by coding Y in the LEASE DATE AFFECTS YIELD switch in the New Lease screen of Portfolio update [U0212]. The first accrual period then begins on the lease date, earlier than the commencement date. Yield is reduced.

For IBL's with Capitalized Interest set to 'I', LeasePak will calculate interest on the interest that is paid after the due date.

Accrual Range

When the Accrual option of the Cycle Accruals update [U0301] is executed interactively, a specific range of payment due days is selected by the user; all leases with a payment due day on or between the specified start and end days are accrued.

When Cycle Accruals is executed through the End of Period process [U04], the accrual process computes the range of payment due days, based on the current date and the last End of Period Cycle Accrual. The start day for the range is the previous cycle accrual's end day plus one. The end day for the range is the current day. All leases with a payment due day on or between the calculated start and end days are accrued for payments due the following month.

If recurring charges are due to accrue and that particular recurring charge is set to use that accrual basis accounting as indicated in U0212 Portfolio → Assessment Customization then LeasePak maintains paid general ledger entry as assessment receivables - recurring charges to debit account and credits assessment income/payables - recurring charges. For accrual basis recurring charges users must own "Accrual Basis Recurring Charges" module.

If recurring charges accruals are in reversal and that particular recurring charge is set to use accrual basis recurring charges accounting as mentioned in U0212 Portfolio → Assessment Customizations then LeasePak maintains the paid general ledger entries as assessment income/payable - RCRs debit and credits assessment receivable - recurring charges.

This screen is used to select the Cycle Accruals update [U0301] option.

Accrual

End of Period: Refer to the End of Period section in this document for information on the corresponding EOP process.

End of Period: Refer to the End of Period section in this document for information on the corresponding EOP process.

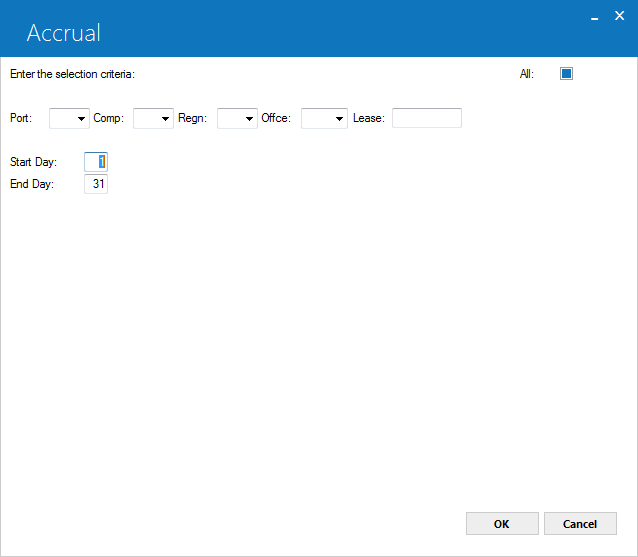

This screen is used to select a lease or group of leases to accrue.

- ALL

Enter X to accrue all leases. Leave blank to accrue a particular portfolio, company, region, office, and/or lease.

- PORT

Enter the number of the portfolio to accrue. Leave blank to accrue across portfolios.

- COMP

Enter the number of the company to accrue. Leave blank to accrue across companies.

- REGN

Enter the number of the region to accrue. Leave blank to accrue across regions.

- OFFIC

Enter the number of the office to accrue. Leave blank to accrue across offices.

- LEASE

Enter the number of the lease to accrue. Leave blank to accrue across leases.

This screen is used to select the range of payment due days for the lease or group of leases to accrue.

The values in the START DAY and END DAY fields are initially defaulted to include all possible payment due days (1 through 31) for lease(s) with monthly accrual/billing cycle, but may be changed to produce a narrower range. If only leases with a particular payment due day are to be accrued, both START DAY and END DAY may be set to the same value. For non-monthly accrual/billing cycle lease(s) U0301 proceed with 1 and 31 as start and end date. The provided date range will be ignored by the system.

NOTE: LeasePak will maintain the accrual and accrual reversal general ledger transaction for the sets/records of subvention general ledger accounts records to accrue subvention income for each set of subvention. LeasePak will generate the following general ledger transactions to accrue subvention income:

Accrue subvention income for lease.

| General Ledger Account | Amount |

| DR IDRD - D/L SUBVENTION1 | Accrual Normal Cycle |

| CR IDRD - D/L SUBVENTION1 INCOME |

To accrue suspended subvention income for a lease that has been suspended using U0115 suspended Earnings.

| General Ledger Account | Amount |

| DR IDRD - D/L SUBVENTION1 | Accrual Normal Cycle |

| CR IDRD - SUSP D/L SUBVENTION1 INC |

To accrue reverse subvention income for lease.

| General Ledger Account | Amount |

| DR IDRD - D/L SUBVENTION1 INCOME | Accrual Reversal Normal |

| CR IDRD - D/L SUBVENTION1 |

To accrue reverse suspended subvention income for a lease that has been suspended using U0115 Suspended Earnings.

| General Ledger Account | Amount |

| DR IDRD - SUSP D/L SUBVENTION1 INC | Accrul Reversal Normal |

| CR IDRD - D/L SUBVENTION1 |

To accrue subvention income for an interest bearing loan.

| General Ledger Account | Amount |

| DR IDRD - RETAIL SUBVENTION1 | Accrual Normal Cycle |

| CR IDRD - RETAIL SUBVENTION1 INC |

To accrue suspended subvention income for an interest bearing loan that has been suspended using U0115 Suspended Earnings.

| General Ledger Account | Amount |

| DR IDRD - RETAIL SUBVENTION1 | Accraul Normal Cycle |

| CR IDRD - SUSP RETAIL SUBVENTION1 INC |

To accrue reverse subvention income for an interest bearing loan.

| General Ledger Account | Amount |

| DR IDRD - RETAIL SUBVENTION1 INC | Accrual Reversal Normal |

| CR IDRD - RETAIL SUBVENTION1 |

To accrue reverse suspended subvention income for an interest bearing loan that has been suspended using U0115 Suspended Earnings.

| General Ledger Account | Amount |

| DR IDRD - SUSP RETAIL SUBVENTION1 | Accrual Reversal Normal |

| CR IDRD - RETAIL SUBVENTION1 |

NOTE: LeasePak produces the following accrual general ledger entries to amortize dealer reserve. To amortize the dealer reserve amount LeasePak will work same as is it does today for IDC3, Fixed Rate Reserve.

Following are the sample general ledger entry used to amortize dealer reserves

Following are the sample general ledger entry is use to amortize dealer reserve for a pre-computed lease:

| General Ledger Account | Amount |

| DR IDC7 - AMORT D/L Dealer RESERVE | Amount - ACCRUAL NORMAL CYCLE |

| CR IDC7 - UNAMORT D/L DEALER RESERVE |

Following sample general ledger entry is use to amortize the dealer bonus for an operating lease:

| General Ledger Account | Amount |

| DR IDC7 - AMORT O/L Dealer RESERVE | Amount - ACCRUAL NORMAL CYCLE |

| CR IDC7 - UNAMORT O/L DEALER RESERVE |

Following sample general ledger entry is used to amortize dealer reserve for an interest-bearing loan:

| General Ledger Account | Amount |

| DR IDC7 - AMORT DEALER RESERVE | Amount - ACCRUAL NORMAL CYCLE |

| CR IDC7 - UNAMORT DEALER RESERVE |

Following are the sample general ledger entry is used to amortize dealer reserve for a pre-computed lease that has been suspended using U0115, Suspended Earnings:

| General Ledger Account | Amount |

| DR IDC7 - D/L SUSP DEALER RESERVE | Amount - ACCRUAL NORMAL CYCLE |

| CR IDC7 - UNAMORT D/L DEALER RESERVE |

Following are the sample general ledger entry is used to amortize dealer reserve for a pre-computed lease that has been suspended using U0115, Suspended Earnings:

| General Ledger Account | Amount |

| DR IDC7 - O/L SUSP DEALER RESERVE | Amount - ACCRUAL NORMAL CYCLE |

| CR IDC7 - UNAMORT O/L DEALER RESERVE |

Following are the sample general ledger entry is used to amortize dealer reserve for an interest bearing-loan lease that has been suspended using U0115, Suspended Earnings:

| General Ledger Account | Amount |

| DR IDC7 - SUSP DEALER RESERVE | Amount - ACCRUAL NORMAL CYCLE |

| CR IDC7 - UNAMORT DEALER RESERVE |

Enhanced IDCs

Following are the general ledger transactions of additional IDC fields (IDC8–IDC9 and IDCA–IDCH) for accruals:

For a precomputed type lease:

| Debit | Credit | ||

| 624 | IDC8 AMORTIZATION | 523 | IDC8–UNAMORT D/L RESERVES |

| 654 | IDC8 – ALT: LEASE INCOME ADJUSTMENT | 527 | ALT:IDC8–UNAMORT RESERVES |

| Debit | Credit | ||

| 625 | IDC9 AMORTIZATION | 531 | IDC9–UNAMORT D/L RESERVES |

| 655 | IDC9 – ALT: LEASE INCOME ADJUSTMENT | 535 | ALT:IDC9–UNAMORT RESERVES |

| Debit | Credit | ||

| 626 | IDCA AMORTIZATION | 539 | IDCA–UNAMORT D/L RESERVES |

| 656 | IDCA – ALT: LEASE INCOME ADJUSTMENT | 543 | ALT:IDCA–UNAMORT RESERVES |

| Debit | Credit | ||

| 627 | IDCB AMORTIZATION | 547 | IDCB–UNAMORT D/L RESERVES |

| 657 | IDCB – ALT: LEASE INCOME ADJUSTMENT | 551 | ALT:IDCB–UNAMORT RESERVES |

| Debit | Credit | ||

| 628 | IDCC AMORTIZATION | 555 | IDCC–UNAMORT D/L RESERVES |

| 658 | IDCC – ALT: LEASE INCOME ADJUSTMENT | 559 | ALT:IDCC–UNAMORT RESERVES |

| Debit | Credit | ||

| 629 | IDCD AMORTIZATION | 563 | IDCD–UNAMORT D/L RESERVES |

| 659 | IDCD – ALT: LEASE INCOME ADJUSTMENT | 567 | ALT:IDCD–UNAMORT RESERVES |

| Debit | Credit | ||

| 630 | IDCE AMORTIZATION | 571 | IDCE–UNAMORT D/L RESERVES |

| 660 | IDCE – ALT: LEASE INCOME ADJUSTMENT | 575 | ALT:IDCE–UNAMORT RESERVES |

| Debit | Credit | ||

| 631 | IDCF AMORTIZATION | 579 | IDCF–UNAMORT D/L RESERVES |

| 661 | IDCF – ALT: LEASE INCOME ADJUSTMENT | 583 | ALT:IDCF–UNAMORT RESERVES |

| Debit | Credit | ||

| 632 | IDCG AMORTIZATION | 587 | IDCG–UNAMORT D/L RESERVES |

| 662 | IDCG – ALT: LEASE INCOME ADJUSTMENT | 591 | ALT:IDCG–UNAMORT RESERVES |

| Debit | Credit | ||

| 633 | IDCH AMORTIZATION | 595 | IDCH–UNAMORT D/L RESERVES |

| 663 | IDCH – ALT: LEASE INCOME ADJUSTMENT | 599 | ALT:IDCH–UNAMORT RESERVES |

For a suspended precomputed type lease:

| Debit | Credit | ||

| 634 | IDC8 – SUSPENDED AMORTIZATION | 523 | IDC8–UNAMORT D/L RESERVES |

| 635 | IDC9 – SUSPENDED AMORTIZATION | 531 | IDC9–UNAMORT D/L RESERVES |

| 636 | IDCA – SUSPENDED AMORTIZATION | 539 | IDCA–UNAMORT D/L RESERVES |

| 637 | IDCB – SUSPENDED AMORTIZATION | 547 | IDCB–UNAMORT D/L RESERVES |

| 638 | IDCC – SUSPENDED AMORTIZATION | 555 | IDCC–UNAMORT D/L RESERVES |

| 639 | IDCD – SUSPENDED AMORTIZATION | 563 | IDCD–UNAMORT D/L RESERVES |

| 640 | IDCE – SUSPENDED AMORTIZATION | 571 | IDCE–UNAMORT D/L RESERVES |

| 641 | IDCF – SUSPENDED AMORTIZATION | 579 | IDCF–UNAMORT D/L RESERVES |

| 642 | IDCG – SUSPENDED AMORTIZATION | 587 | IDCG–UNAMORT D/L RESERVES |

| 643 | IDCH – SUSPENDED AMORTIZATION | 595 | IDCH–UNAMORT D/L RESERVES |

For an operating type lease:

| Debit | Credit | ||

| 624 | IDC8 AMORTIZATION | 525 | IDC8–UNAMORT D/L–O/L RESERVES |

| 654 | IDC8 – ALT: LEASE INCOME ADJUSTMENT | 527 | ALT:IDC8–UNAMORT RESERVES |

| Debit | Credit | ||

| 625 | IDC9 AMORTIZATION | 533 | IDC9–UNAMORT D/L–O/L RESERVES |

| 655 | IDC9 – ALT: LEASE INCOME ADJUSTMENT | 535 | ALT:IDC9–UNAMORT RESERVES |

| Debit | Credit | ||

| 626 | IDCA AMORTIZATION | 541 | IDCA–UNAMORT D/L–O/L RESERVES |

| 656 | IDCA – ALT: LEASE INCOME ADJUSTMENT | 543 | ALT:IDCA–UNAMORT RESERVES |

| Debit | Credit | ||

| 627 | IDCB AMORTIZATION | 549 | IDCB–UNAMORT D/L–O/L RESERVES |

| 657 | IDCB – ALT: LEASE INCOME ADJUSTMENT | 551 | ALT:IDCB–UNAMORT RESERVES |

| Debit | Credit | ||

| 628 | IDCC AMORTIZATION | 557 | IDCC–UNAMORT D/L–O/L RESERVES |

| 658 | IDCC – ALT: LEASE INCOME ADJUSTMENT | 559 | ALT:IDCC–UNAMORT RESERVES |

| Debit | Credit | ||

| 629 | IDCD AMORTIZATION | 565 | IDCD–UNAMORT D/L–O/L RESERVES |

| 659 | IDCD – ALT: LEASE INCOME ADJUSTMENT | 567 | ALT:IDCD–UNAMORT RESERVES |

| Debit | Credit | ||

| 630 | IDCE AMORTIZATION | 573 | IDCE–UNAMORT D/L–O/L RESERVES |

| 660 | IDCE – ALT: LEASE INCOME ADJUSTMENT | 575 | ALT:IDCE–UNAMORT RESERVES |

| Debit | Credit | ||

| 631 | IDCF AMORTIZATION | 581 | IDCF–UNAMORT D/L–O/L RESERVES |

| 661 | IDCF – ALT: LEASE INCOME ADJUSTMENT | 583 | ALT:IDCF–UNAMORT RESERVES |

| Debit | Credit | ||

| 632 | IDCG AMORTIZATION | 589 | IDCG–UNAMORT D/L–O/L RESERVES |

| 662 | IDCG – ALT: LEASE INCOME ADJUSTMENT | 591 | ALT:IDCG–UNAMORT RESERVES |

| Debit | Credit | ||

| 633 | IDCH AMORTIZATION | 597 | IDCH–UNAMORT D/L–O/L RESERVES |

| 663 | IDCH – ALT: LEASE INCOME ADJUSTMENT | 599 | ALT:IDCH–UNAMORT RESERVES |

For a suspended operating lease:

| Debit | Credit | ||

| 634 | IDC8 – SUSPENDED AMORTIZATION | 525 | IDC8–UNAMORT D/L–O/L RESERVES |

| 635 | IDC9 – SUSPENDED AMORTIZATION | 533 | IDC9–UNAMORT D/L–O/L RESERVES |

| 636 | IDCA – SUSPENDED AMORTIZATION | 541 | IDCA–UNAMORT D/L–O/L RESERVES |

| 637 | IDCB – SUSPENDED AMORTIZATION | 549 | IDCB–UNAMORT D/L–O/L RESERVES |

| 638 | IDCC – SUSPENDED AMORTIZATION | 557 | IDCC–UNAMORT D/L–O/L RESERVES |

| 639 | IDCD – SUSPENDED AMORTIZATION | 565 | IDCD–UNAMORT D/L–O/L RESERVES |

| 640 | IDCE – SUSPENDED AMORTIZATION | 573 | IDCE–UNAMORT D/L–O/L RESERVES |

| 641 | IDCF – SUSPENDED AMORTIZATION | 581 | IDCF–UNAMORT D/L–O/L RESERVES |

| 642 | IDCG – SUSPENDED AMORTIZATION | 589 | IDCG–UNAMORT D/L–O/L RESERVES |

| 643 | IDCH – SUSPENDED AMORTIZATION | 597 | IDCH–UNAMORT D/L–O/L RESERVES |

For an interest–bearing loan:

| Debit | Credit | ||

| 604 | IDC8 – FASB91 INCOME ADJUSTMENT | 521 | IDC8–UNAMORTIZED RESERVES |

| 654 | IDC8 – ALT: LEASE INCOME ADJUSTMENT | 527 | ALT:IDC8–UNAMORT RESERVES |

| Debit | Credit | ||

| 605 | IDC9 – FASB91 INCOME ADJUSTMENT | 529 | IDC9–UNAMORTIZED RESERVES |

| 655 | IDC9 – ALT: LEASE INCOME ADJUSTMENT | 535 | ALT:IDC9–UNAMORT RESERVES |

| Debit | Credit | ||

| 606 | IDCA – FASB91 INCOME ADJUSTMENT | 537 | IDCA–UNAMORTIZED RESERVES |

| 656 | IDCA – ALT: LEASE INCOME ADJUSTMENT | 543 | ALT:IDCA–UNAMORT RESERVES |

| Debit | Credit | ||

| 607 | IDCB – FASB91 INCOME ADJUSTMENT | 545 | IDCB–UNAMORTIZED RESERVES |

| 657 | IDCB – ALT: LEASE INCOME ADJUSTMENT | 551 | ALT:IDCB–UNAMORT RESERVES |

| Debit | Credit | ||

| 608 | IDCC – FASB91 INCOME ADJUSTMENT | 553 | IDCC–UNAMORTIZED RESERVES |

| 658 | IDCC – ALT: LEASE INCOME ADJUSTMENT | 559 | ALT:IDCC–UNAMORT RESERVES |

| Debit | Credit | ||

| 609 | IDCD – FASB91 INCOME ADJUSTMENT | 561 | IDCD–UNAMORTIZED RESERVES |

| 659 | IDCD – ALT: LEASE INCOME ADJUSTMENT | 567 | ALT:IDCD–UNAMORT RESERVES |

| Debit | Credit | ||

| 610 | IDCE – FASB91 INCOME ADJUSTMENT | 569 | IDCE–UNAMORTIZED RESERVES |

| 660 | IDCE – ALT: LEASE INCOME ADJUSTMENT | 575 | ALT:IDCE–UNAMORT RESERVES |

| Debit | Credit | ||

| 611 | IDCF – FASB91 INCOME ADJUSTMENT | 577 | IDCF–UNAMORTIZED RESERVES |

| 661 | IDCF – ALT: LEASE INCOME ADJUSTMENT | 583 | ALT:IDCF–UNAMORT RESERVES |

| Debit | Credit | ||

| 612 | IDCG – FASB91 INCOME ADJUSTMENT | 585 | IDCG–UNAMORTIZED RESERVES |

| 662 | IDCG – ALT: LEASE INCOME ADJUSTMENT | 591 | ALT:IDCG–UNAMORT RESERVES |

| Debit | Credit | ||

| 613 | IDCH – FASB91 INCOME ADJUSTMENT | 593 | IDCH–UNAMORTIZED RESERVES |

| 663 | IDCH – ALT: LEASE INCOME ADJUSTMENT | 599 | ALT:IDCH–UNAMORT RESERVES |

For a suspended interest–bearing loan:

| Debit | Credit | ||

| 614 | IDC8 – SUSP FASB91 INCOME ADJUSTMENT | 521 | IDC8–UNAMORTIZED RESERVES |

| 615 | IDC9 – SUSP FASB91 INCOME ADJUSTMENT | 529 | IDC9–UNAMORTIZED RESERVES |

| 616 | IDCA – SUSP FASB91 INCOME ADJUSTMENT | 537 | IDCA–UNAMORTIZED RESERVES |

| 617 | IDCB – SUSP FASB91 INCOME ADJUSTMENT | 545 | IDCB–UNAMORTIZED RESERVES |

| 618 | IDCC – SUSP FASB91 INCOME ADJUSTMENT | 553 | IDCC–UNAMORTIZED RESERVES |

| 619 | IDCD – SUSP FASB91 INCOME ADJUSTMENT | 561 | IDCD–UNAMORTIZED RESERVES |

| 620 | IDCE – SUSP FASB91 INCOME ADJUSTMENT | 569 | IDCE–UNAMORTIZED RESERVES |

| 621 | IDCF – SUSP FASB91 INCOME ADJUSTMENT | 577 | IDCF–UNAMORTIZED RESERVES |

| 622 | IDCG – SUSP FASB91 INCOME ADJUSTMENT | 585 | IDCG–UNAMORTIZED RESERVES |

| 623 | IDCH – SUSP FASB91 INCOME ADJUSTMENT | 593 | IDCH-UNAMORTIZED RESERVES |

U0301 Accrual produces the following general ledger transaction for the amount of IDC ASC 842 if the IDC ASC 842 accounting method (I/A/B) is set to 'A' – AMOR or 'B' – AMR2.

When lease is at Active status:

| Debit | Credit | ||

| 669 | IDC AMORTIZATION - ASC 842 | 666 | UNAMORTIZED IDC COST - ASC 842 |

When lease status is suspended:

| Debit | Credit | ||

| 667 | SUSPENDED IDC ACCRUED - ASC 842 | 666 | UNAMORTIZED IDC COST - ASC 842 |

Following are the general ledger transactions when Prorate Incomer IDC/IDR field is set to 'Y' from U0212 Portfolio → Miscellaneous Customizations.

When lease is at Active status:

| Debit | Credit | ||

| 670 | DEFERRED IDC AMORTIZATION - ASC 842 | 666 | UNAMORTIZED IDC COST - ASC 842 |

| 669 | IDC AMORTIZATION - ASC 842 | 670 | DEFERRED IDC AMORTIZATION - ASC 842 |

When lease status is suspended:

| Debit | Credit | ||

| 669 | IDC AMORTIZATION – ASC 842 | 670 | DEFERRED IDC AMORTIZATION – ASC 842 |

| 671 | DEFERRED SUSP IDC ACCRUED – ASC 842 | 666 | UNAMORTIZED IDC COST – ASC 842 |

| 667 | SUSPENDED IDC ACCRUED – ASC 842 | 671 | DEFERRED SUSP IDC ACCRUED – ASC 842 |

For other leases to continue amortizing the unamortized IDC/IDR amounts, U0301 Accrual update will determine which IDCs and IDRs to accrue by lease Book IDC accounting method (I/A/B), IDC1-9, IDCA-H accounting method (I/A/B), and IDR1-9, IDRA-H accounting method (I/A/B).

AOPM/ROPM Accrual Method

Following are the general ledger transactions for leases that have not matured and extended with accrual base (A) lease extension accounting method:

| Debit | Credit | ||

| 60 | DEFERRED OPER LEASE REVENUE | 82 | OPERATING LEASE INCOME |

| 3 | LEASE PAYMENTS RECEIVABLE | 60 | DEFERRED OPER LEASE REVENUE |

| 60 | DEFERRED OPER LEASE REVENUE | 82 | OPERATING LEASE INCOME |

If the lease status is suspended:

| Debit | Credit | ||

| 40 | SUSPENDED RECIEVABLE (INCOME) | 60 | DEFERRED OPER LEASE RVENUE |

| 60 | DEFERRED OPER LEASE REVENUE | 103 | SUSPENDED INCOME ACCRUED |

LeasePak maintains the following general ledger transactions to clear the remaining balance if there are no more schedule payments to accrue and there is a remaining amount in "Deferred Operating Lease Revenue" general ledger account:

| Debit | Credit | ||

| 60 | DEFERRED OPER LEASE REVENUE | 82 | OPERATING LEASE INCOME |

If the lease status is suspended:

| Debit | Credit | ||

| 60 | DEFERRED OPER LEASE REVENUE | 103 | SUSPENDED INCOME ACCRUED |

ARES/RRES Accrual Method

The *RES lease accrual method will recognize income after the residual value on the lease has been reduced to 0 by the scheduled payment amount on an extended lease. Any excess payments that are accrued will be income. Following are the general ledger transactions.

Following are the general ledger transactions for leases that have matured and extended with accrual base (A) lease extension accounting method:

| Debit | Credit | ||

| 3 | LEASE PAYMENTS RECEIVABLE | 5 | LEASE INCOME RECEIVABLE |

| 5 | LEASE INCOME RECEIVABLE | 284 | DEFERRED LESSOR INCOME - PRE |

| 5 | LEASE INCOME RECEIVABLE | 80 | LESSOR INCOME - PRECOMPUTED |

If the lease status is suspended:

| Debit | Credit | ||

| 40 | SUSPENDED RECEIVABLE (INCOME) | 42 | SUSPENDED INCOME RECV (UNBILLED) |

| 42 | SUSPENDED INCOME RECV (UNBILLED) | 103 | SUSPENDED INCOME ACCRUED |

| 42 | SUSPENDED INCOME RECV (UNBILLED) | 286 | DEFERRED SUSP INCOME ACCRUED |

| 284 | DEFERRED LESSOR INCOME - PRE | 80 | LESSOR INCOME - PRECOMPUTED |

LeasePak maintains the following general ledger transactions to clear the remaining balance if there are no more schedule payments to accrue, and there is a remaining amount in the "Deferred Lessor Income - Pre" general ledger account:

| Debit | Credit | ||

| 284 | DEFERRED LESSOR INCOME - Pre | 80 | LESSOR INCOME - PRECOMPUTED |

If the lease status is suspended:

| Debit | Credit | ||

| 286 | DEFERRED SUSP INCOME ACCRUED | 103 | SUSPENDED INCOME ACCRUED |

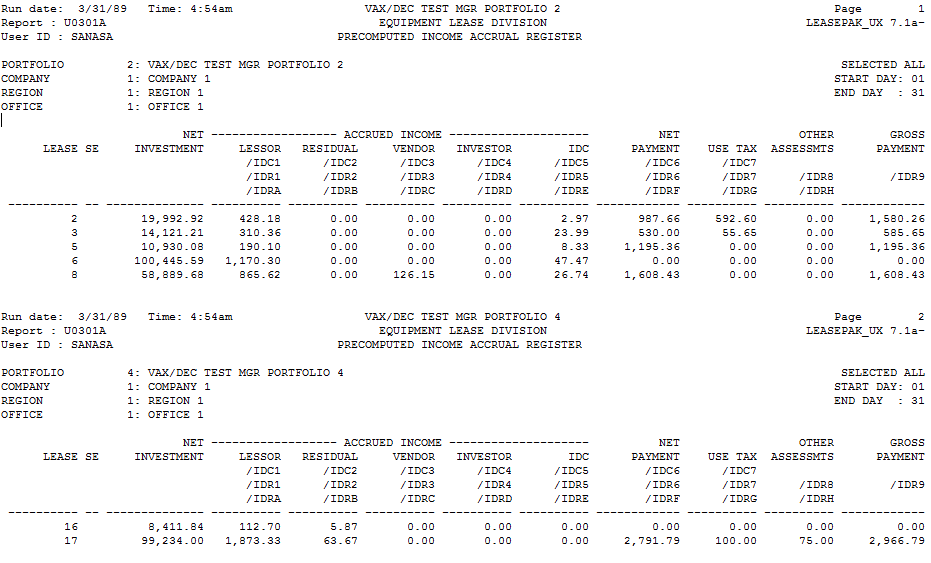

Cycle Accrual Audit - Precomputed Income Accrual Register

The Cycle Accrual Audit report [U0301A] reports at the lease level and provides the following income accrual information for each precomputed interest lease accrued:

- LEASE

The number of the lease accrued is displayed.

- SE

This column designates if a lease is in suspended earnings status or is extended. An asterisk (*) is displayed if the lease is in a suspended earnings status. An R is displayed if the lease has been extended using the RES method on a cash basis.

- NET INVESTMENT

The net investment of the lease after the accrual process is displayed.

- LESSOR ACCRUED INCOME

The amount of income accrued to the lessor is displayed. If the lease has been extended using the RES method on a cash basis, this amount represents the amount of deferred income.If more than one month is accrued, each month's income accrual is shown on a separate line, up to a maximum of 10 months. If more than 10 months are accrued, the first 9 months' income accruals are shown and the remaining accruals are accumulated in the tenth line.

- RESIDUAL

ACCRUED INCOME

The amount of residual income accrued is displayed. See Note above. If the lease has been extended using the RES method on a cash basis, this amount represents the amount of deferred residual.

- VENDOR

ACCRUED INCOME

The amount of income accrued to the vendor is displayed. See Note above.

- INVESTOR ACCRUED INCOME

The amount of income accrued to the investor is displayed. See Note above.

- IDC

ACCRUED INCOME

The amount of initial direct costs (IDC) amortized is displayed. See Note above.

- ITC ACCRUED

INCOME

The amount of income accrued for investment tax credit (ITC) is displayed. See Note above.

- NET PAYMENT

The lease payment for each month accrued, not including use tax, is displayed.

- USE TAX

The use tax for the lease payment for each month accrued is displayed. If the Sales Tax On Assessment module is purchased, this will also include any sales tax calculated for recurring charges or other assessments.

- OTHER ASSESSMNTS

The total amount of other assessment charges for each month accrued is displayed. OTHER ASSESSMENTS are recurring charges or late charges.

- GROSS PAYMENT

The total payment is displayed. It is calculated as follows: - IDC1

The total amount for IDC 1- Insurance Premium, is displayed.

NET PAYMENT

+ USE TAX

+ OTHER ASSESSMENTS

- IDC2

The total amount for IDC 2 - Notary Fee, is displayed.

- IDC 3

The total amount for IDC 3- Fixed Rate Reserves, is displayed.

- IDC4

The total amount for IDC 4- Standard Reserves, is displayed.

- IDC5

The total amount for IDC 5- Guaranteed Reserves, is displayed.

- IDR1

The total amount for IDR 1- Insurance Fees, is displayed.

- IDR 2

The total amount for IDR 2- Registration Fees, is displayed.

- IDR3

The total amount for IDR 3- Vendor Subsidy, is displayed.

- IDR 4

The total amount for IDR 4- Opening Commission is displayed.

- IDR5

The total amount for IDR 5-Subvention, is displayed.

- IDR 6

The total amount for IDR 6-Dealer Buy Down, is displayed.

- IDR7

The total amount for IDR 7-Credit Life Insurance 1, is displayed.

- IDR8

The total amount for IDR 8- Credit life Insurance 2, is displayed.

- IDR9

The total amount for IDR 9- Credit Disability Insurance 1, is displayed.

- IDRA

The total amount for IDR A-Credit Disability Insurance 2, is displayed.

- IDRB

The total amount for IDR B- Acquisition Fee, is displayed.

- IDRC

The total amount for IDR C- Warranty Insurance Fee, is displayed.When the Enhanced IDC/IDR module is purchased, LeasePak will display the IDC/IDRs totals.

When accruals or accrual reversals are being run for the first time with the new IDC/IDRs, the first lease with IDC/IDR fees may be $0.01 less than the amortization schedule generated. The penny difference will be recognized when all IDC/IDR's are fully amortized.

- TOTALS

The totals for each column show the total amount for active leases, the total amount for leases in a suspended earnings status, the total amount for leases extended on a cash basis (deferred), and the combined total for all 3. The numbers of active leases, suspended leases and deferred leases are displayed.

- SUBVENTION 1

The total amount for subvention 1 is displayed.

- SUBVENTION 2

The total amount for subvention 2 is displayed.

- SUBVENTION 3

The total amount for subvention 3 is displayed.

- SUBVENTION 4

The total amount for subvention 4 is displayed.

- SUBVENTION 5

The total amount for subvention 5 is displayed.

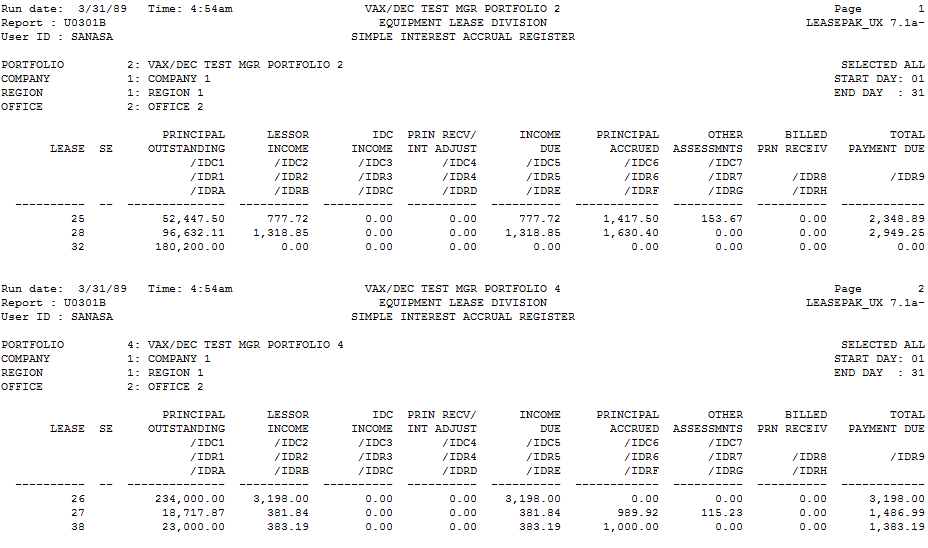

Cycle Accrual Audit - Simple Interest Accrual Register

The Cycle Accrual Audit report [U0301B] reports at the lease level and provides the following income accrual information for each simple interest lease accrued:

- LEASE

The number of the lease accrued is displayed.

- SUSPND

EARNGS

An asterisk (*) is displayed if the lease is in a suspended earnings status.

- PRINCIPAL

OUTSTANDING

The principal outstanding of the lease after the accrual process is displayed.

- LESSOR

ACCRUED INCOME

The amount of income accrued to the lessor is displayed. If more than one month is accrued, each month's income accrual is shown on a separate line, up to a maximum of 10 months. If more than 10 months are accrued, the first 9 months' income accruals are shown and the remaining accruals are accumulated in the tenth line.

- PRIN RECV/INT ADJUST

For floating rate simple interest leases with constant payments (LT accrual method only), the difference between the level payment and the actual payment due for each month accrued is displayed. Differences occur because of changes in the base rate from the original (quoted) lease rate. This value may be positive or negative. A positive value indicates the base rate has risen, compared to the original rate and therefore, the lessee actually owes more than the established constant payment. A negative value indicates the base rate has fallen, and therefore, the lessee actually owes less than the established constant payment.

For floating rate simple interest leases with variable payments (VV and VL accrual methods only), the interest adjustment due to fluctuations in the previous accrual's base rate is displayed. An interest adjustment is necessary, because accruals are calculated in advance and, therefore, projected base rates must be used. The next period's income accrual must adjust the last period's projected income accrued, if the actual base rate for the last period differs from the projected base rate.For example, assume on January 1 the accrual process executes for payments due on February 1, and the interest accrued for the period of January 1 through January 31 is $100 based on a projected base rate of 10%. On February 1, the actual base rate for the period of January 1 through January 31 is 9%, which results in an actual interest amount of $90. The interest adjustment displayed for the period is $10.

- INCOME

DUE

The income due for each month accrued is displayed.

- PRINCIPAL

ACCRUED

The principal portion of the payment for each month accrued is displayed.

- OTHER ASSESSMNTS

The total amount of other assessment charges for each month accrued is displayed. OTHER ASSESSMENTS are recurring charges or late charges.

- BILLED PRN RECEIV

For floating rate simple interest leases with constant payments (LT accrual method only), the last period adjustment for overages or shortages due to fluctuations in the base rate from the original (quoted) rate is displayed. This value is only shown if the lease has matured.

- TOTAL

PAYMENT DUE

The total lease payment due is displayed. It is calculated as follows:PRINCIPAL ACCRUED

+ INCOME DUE

+ OTHER ASSESSMENTS

+ PRINCIPAL RECEIV (LT method only)

+ BILLED PRIN RECV (LT method only) - TOTALS

The totals for each column show the total amount for active leases, the total amount for leases in a suspended earnings status, and the combined total for both. The numbers of active leases and suspended leases are displayed.

- SUBVENTION 1

The total amount for subvention 1 is displayed.

- SUBVENTION 2

The total amount for subvention 2 is displayed.

- SUBVENTION 3

The total amount for subvention 3 is displayed.

- SUBVENTION 4

The total amount for subvention 4 is displayed.

- SUBVENTION 5

The total amount for subvention 5 is displayed.

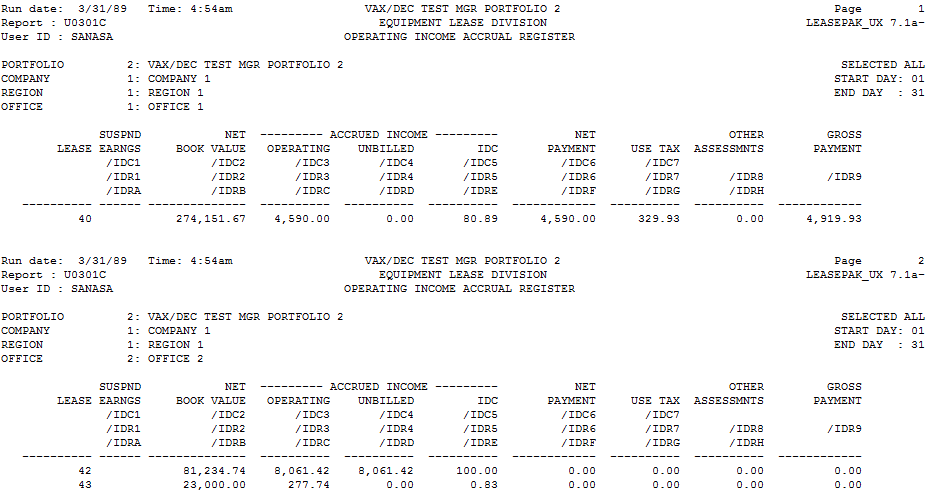

Cycle Accrual Audit - Operating Income Accrual Register

The Cycle Accrual Audit report [U0301C] reports at the lease level and provides the following income accrual information for each operating lease accrued:

- LEASE

The number of the lease accrued is displayed.

- SUSPND

EARNGS

An asterisk (*) is displayed if the lease is in a suspended earnings status.

- NET BOOK VALUE

The current net book value of the lease is displayed. The net book value is calculated as: - ACCRUED

INCOME OPERATING

The amount of operating income accrued to the lessor is displayed.If more than one month is accrued, each month's income accrual is shown on a separate line, up to a maximum of 10 months. If more than 10 months are accrued, the first 9 months' income accruals are shown and the remaining accruals are accumulated in the tenth line.

LEASED ASSETS - ACCUMULATED DEPRECIATION

- SUBVENTION 1

The total amount for subvention 1 is displayed.

- SUBVENTION 2

The total amount for subvention 2 is displayed.

- SUBVENTION 3

The total amount for subvention 3 is displayed.

- SUBVENTION 4

The total amount for subvention 4 is displayed.

- SUBVENTION 5

The total amount for subvention 5 is displayed.

- ACCRUED

INCOME UNBILLED

The amount of unbilled operating income accrued to the lessor is displayed. Unbilled operating income is the difference between the amount accrued on a straight-line basis and the amount due. See Note above.

- IDC

ACCRUED INCOME

The amount of initial direct costs (IDC) amortized is displayed. See Note above.

- NET PAYMENT

The lease payment for each accrual month, not including use tax, is displayed.

- USE TAX

The use tax for the lease payment for each accrual month is displayed. If the Sales Tax On Assessment module is purchased, this will also include any sales tax calculated for recurring charges or other assessments.

- OTHER ASSESSMENTS

The total amount of other assessment charges for each accrual month is displayed.

- GROSS

PAYMENT

The total payment is displayed. It is calculated as follows:NET PAYMENT

+ USE TAX

+ OTHER ASSESSMENTS - TOTALS

The totals for each column show the total amount for active leases, the total amount for leases in a suspended earnings status, and the combined total for both. The numbers of active leases and suspended leases are displayed.

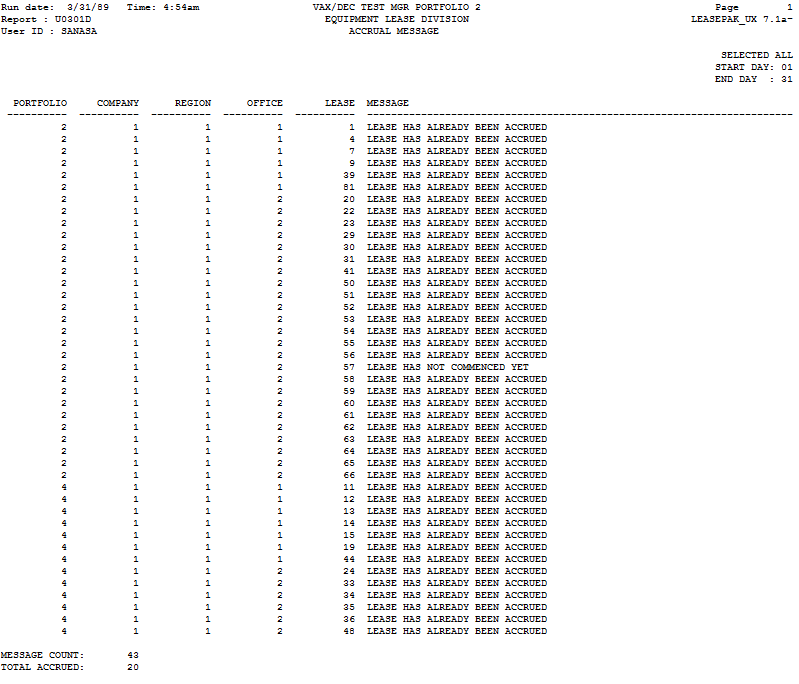

Cycle Accrual Exception - Accrual Message

The Cycle Accrual Exception report [U0301D] reports at the lease level and displays messages on the status of accrual processing.

- PORTFOLIO/COMPANY/REGION/OFFICE/LEASE

The P/C/R/O and lease number are displayed.

- MESSAGE

Most messages indicate that the lease did not accrue (except those which specifically state that the accrual did complete). After accrual, each message appearing on this report should be examined and corrective action should be taken immediately, where warranted. Possible accrual messages and their meanings (in alphabetical order) are:ACCRUAL TYPES ARE NOT ALL APR

If one lessor, vendor, or investor accrual method for a lease is AAPR or RAPR, then all accrual methods must be of that type. This message indicates a data error. Notify your client services representative at NetSol.BASE RATES DO NOT EXIST FOR THE LEASE

This message is used for floating rate interest accruals only. It means that no record was found on the Base Rates (RPR) file for the base rate code for the lease. Reconfirm base rate code for the lease through the Master Financial update [U0202] and the base rates on the Base Rates (RPR) file through the Base Rates update [U0705].ERROR ENCOUNTERED DURING USE TAX ACCRUAL

Use tax could not be accrued for the lease because:

The record(s) on the Asset (REQ) file could not be found for the lease. This message indicates a possible data error. In this case, notify your client services representative at NetSol.

The record(s) on the Location (RLO) file could not be found for the lease. It is likely that the location record(s) were deleted through the Location update [U0701]. In this case, assess the use tax manually through the Assessment update [U0105], and re-add the location to the Location (DLO) file using the Location update [U0701] or change the location of the asset through the Asset update [U0210].

ERROR

IN NEXT PAYMENT DUE DATE. PLEASE NOTIFY NETSOL TECHNOLOGIES INC.

The next payment

due date for the lease is not correct. This message indicates a data error. Notify

your client services representative at NetSol.

ERROR

LIMIT (10,000) REACHED. PROCESSING HALTED.

The maximum number of messages

and/or errors (10,000) has been reached. Leases after the Portfolio/Company/Region/Office/Lease

number shown on the report were not accrued, and should be accrued interactively

using this update. If an invoicing run was also performed, the invoices for the

unaccrued leases do not show any payments scheduled to be accrued by this cycle.

Therefore, invoices should be regenerated using the Cycle Invoices update [U0302]

once the leases are interactively accrued.

GENERAL

LEDGER RECORD DOES NOT EXIST FOR THE OFFICE

The record for the office of the

lease was not found on the General Ledger (RGL) file. This message indicates a

data error. Notify your client services representative at NetSol.

IBL

HAS NEGATIVELY AMORTIZED BY $000,000.00 (PRN = $000,000,000.00)

A P&I

interest bearing loan has negatively amortized (interest amount due is greater

than the scheduled loan payment). The amount of the negative amortization (for

the current month only) is shown, as well as the new principal balance (including

the negative amortization amount). This message is informational only.

IBL

NET OUTSTNDG OF $000,000,000.00 > TARGET PRN BAL OF $000,000,000.00

The

net outstanding calculation (as defined through the Custom Calculations option

of the Portfolio update [U0212]) does not meet the target principal balance established

for this interest bearing loan. Target principal balances are set up during New

Lease booking and may be modified through the Master Financial maintenance update

[U0202]. This message is informational only.

LEASE

HAS ALREADY BEEN ACCRUED

The lease has already been accrued to its current

point. This message is informational only, and no action is needed.

LEASE

HAS BEEN TERMINATED EARLY

This message is used for floating rate/level lease

payments interest accrual only (LT accrual methods). It is informational and indicates

that the lease has matured earlier than its scheduled term due to a large build-up

in negative principal receivable. That is, the actual interest rate over the life

of the lease is considerably less than the scheduled interest rate, thereby allowing

the lessee to payoff earlier than scheduled. No refund of negative principal receivable

is required.

LEASE

HAS TERMINATED EARLY AND SOME MONEY MUST BE REFUNDED

This message is used

for floating rate/level lease payments interest accrual only (LT accrual methods).

It is informational and indicates that the lease has matured earlier than scheduled

and some negative principal receivable must be refunded to the lessee.

LEASE

IN GROUP CANNOT BE FOUND

The next lease in the group cannot be found. This

message indicates a data error. Notify your client services representative at

NetSol.

SOME MONEY

MUST BE REFUNDED ON THIS LEASE

This message is used for floating rate/level

lease payments interest accrual only (LT accrual methods). It is informational

and indicates that the lease has matured and some negative principal receivable

must be refunded to the lessee.

STATES

RECORD DOES NOT EXIST

This message is used for floating rate interest accrual.

It indicates that the state for the lessee's address does not exist on the State

(RST) file. Check the lessee's state using the Lessee update [U0203]. If the address

contains the correct state, use the State update [U0713] to see if the state exists

on the State (RST) file. NetSol provides a full State (RST) file at the initial installation.

It is maintained by the user.

TRANSACTION

IS IN PROGRESS

This message indicates that either the End of Period process

[U04] is already submitted for the portfolio or that a data file or record needed

for the accrual process is found to be locked by another user. Check to see if

the accrual process completed successfully.

UNABLE

TO ACCESS LEASE

This message indicates that the record for the lease on the

Master Financial (RLS) file is locked. Try executing the Cycle Accruals update

[U0301] for the lease again. This message should not appear if executing through

End of Period.

UNSUCCESSFUL

ACCESS OF NEXT UNLOCKED PORTFOLIO

This message appears only when executing

accruals interactively across portfolios. The program tried to access the portfolio

and failed because End of Period [U04] was submitted for the portfolio. During

the End of Period process [U04] the updates for the portfolio are locked. The

accrual process skips over the inaccessible portfolio and continues with the next

portfolio.

UNSUCCESSFUL

BEGIN TRANSACTION FOR FINAL UPDATING

This message indicates that initialization

is required before the final updating section may be completed. Final updating

is done to the End of Period (RAS) file if executing through End of Period or

the Operator (ROP) file if executing interactively. Contact your client services

representative at NetSol if this error occurs.

Totals for the Cycle Accrual Exception report [U0301D] show:

- MESSAGE COUNT

- TOTAL ACCRUED

End of Period

| EOP Only | No |

| Frequency | Predefined cycle |

| Sequential Updates | Yes |

| Skip Notes | See comments below |

For more information about End of Period, refer to U04 End of Period Overview.

For more information about End of Period, refer to U04 End of Period Overview.

Sequential Updates: This EOP module runs as part of U0411 Sequential Updates.

Sequential Updates: This EOP module runs as part of U0411 Sequential Updates.

This module is the same update that may be executed interactively through the Cycle Accrual update [U0301]. It accrues income, transfers long-term receivables to current receivables, and calculates and assesses use tax. Reports for each accrual category (precomputed, simple, and operating) are produced which show information on the leases accrued. Another report is produced which lists any messages and/or errors encountered during the accrual process.

Skip Notes: If this module is skipped, then both the Cycle Invoices update [U0302] and the Cycle Invoices (Formatting) update [U0457] should also be skipped. If they are not skipped, the End of Period Cycle Invoices do not invoice current charges for the group of leases that did not accrue. This group of leases is automatically accrued during the next End of Period Cycle Accrual.

The difference between the interactive Cycle Accrual update and the End of Period Cycle Accrual update is that the latter automatically determines the appropriate leases to accrue, whereas, in the former, the leases to accrue are specified by the user. This automatic determination is made using 3 items:

- The accrual deferral days at the portfolio level (specified through the ACCRUAL DEFERRAL DAYS parameter found on

the second screen of the Miscellaneous Customizations option of the Portfolio update [U0212]),

- The accrual cycle (specified through the Predefined Cycles Customization option of the Portfolio update [U0212]), and

- An internal calendar maintained by LeasePak which stores information about the last End of Period accrual process.

In automatically determining the appropriate leases to accrue for a particular End of Period, LeasePak calculates a starting day and an ending day. All leases with due days on or between these starting and ending days are accrued. The starting day for a particular End of Period Cycle Accrual is calculated as:

ENDING DAY OF THE LAST END OF PERIOD CYCLE ACCRUAL + ONE DAY

If the starting day calculation is greater than 31, it is set to 1. The ending day for a particular End of Period Cycle Accrual is calculated as:

CURRENT ACCRUAL CYCLE - ACCRUAL DEFERRAL DAYS (portfolio level)

If the ending day calculation is zero, the number 31 is added to it. If the ending day calculation is negative, the number of days in the previous month is added to it. For example, if the current cycle accrual is March 9, and there is a 10 day accrual deferral period, the ending day calculation is as follows:

9 - 10 + 28 = 27 (assuming 28 days in February)

In this way, short months are handled automatically. For example, to determine the cycle accrual for any given day assume:

- The accrual cycle is every day of the month (i.e., payments may be due on any day of the month),

- The accrual deferral days at the portfolio level is 10 days.

The following dates would have the following accrual cycles:

| Date | Cycle | Date | Cycle |

|---|---|---|---|

| 02/01/95 | 22 | 02/22/95 | 12 |

| 02/02/95 | 23 | 02/23/95 | 13 |

| 02/03/95 | 24 | 02/24/95 | 14 |

| 02/04/95 | 25 | 02/25/95 | 15 |

| 02/05/95 | 26 | 02/26/95 | 16 |

| 02/06/95 | 27 | 02/27/95 | 17 |

| 02/07/95 | 28 | 02/28/95 | 18 |

| 02/08/95 | 29 | 03/01/95 | 19 |

| 02/09/95 | 30 | 03/02/95 | 20 |

| 02/10/95 | 31 | 03/03/95 | 21 |

| 02/11/95 | 1 | 03/04/95 | 22 |

| 02/12/95 | 2 | 03/05/95 | 23 |

| 02/13/95 | 3 | 03/06/95 | 24 |

| 02/14/95 | 4 | 03/07/95 | 25 |

| 02/15/95 | 5 | 03/08/95 | 26 |

| 02/16/95 | 6 | 03/09/95 | 27 |

| 02/17/95 | 7 | 03/10/95 | 28 - 31 |

| 02/18/95 | 8 | 03/11/95 | 1 |

| 02/19/95 | 9 | 03/12/95 | 2 |

| 02/20/95 | 10 | . | |

| 02/21/95 | 11 | . |

To illustrate the automatic accrual cycle determination, assume the following information:

- The accrual deferral days at the portfolio level is 10 days,

- The accrual cycle is 10, 20 and 30 (i.e., payments may be due on any of these three days of the month),

- The ending day of the last End of Period Cycle Accrual is 30,

- The current date is the 20th of the month.

The starting day of the End of Period Cycle Accrual is the ending day of the last End of Period Cycle Accrual plus one:

STARTING DAY = 30 + 1 = 31

The ending day of the End of Period Cycle Accrual is the current accrual cycle less the accrual deferral days at the portfolio level:

ENDING DAY = 20 - 10 = 10

Therefore, leases with payment due days between the 31st of the previous month and the 10th of the current month are accrued.

Continuing this same example, assume the End of Period Cycle Accrual as shown in example 1 completes and it is now ten days later. The starting information is now:

- The accrual deferral days at the portfolio level is 10 days (same as before),

- The accrual cycle is 10, 20 and 30 (same as before),

- The ending day of the last End of Period Cycle Accrual is 10,

- The current date is the 30th of the month.

The starting day of the End of Period Cycle Accrual is the ending day of the last End of Period Cycle Accrual plus one:

STARTING DAY = 10 + 1 = 11

The ending day of the End of Period Cycle Accrual is the current accrual cycle less the accrual deferral days at the portfolio level:

ENDING DAY = 30 - 10 = 20

Therefore, leases with payment due days between the 11th and the 20th of the current month are accrued.

Continuing this same example one step further, assume the End of Period Cycle Accrual as shown in example 2 completes and it is an additional 10 days later. The starting information is now:

- The accrual deferral days at the portfolio level is 10 days (same as before),

- The accrual cycle is 10, 20 and 30 (same as before),

- The ending day of the last End of Period Cycle Accrual is 20,

- The current date is the 10th of the month.

The starting day of the End of Period Cycle Accrual is the ending day of the last End of Period Cycle Accrual plus one:

STARTING DAY = 20 + 1 = 21

The ending day of the End of Period Cycle Accrual is the current accrual cycle less the accrual deferral days at the portfolio level, adjusted by 31 if the resulting value is zero or negative:

ENDING DAY = 10 - 10 = 0 + 31 = 31

Therefore, leases with payment due days between the 21st and the 31st of the current month are accrued.

Continuing this same example one more step to show the complete cycle, assume the End of Period Cycle Accrual as shown in example 3 completes and it is an additional 10 days later. The starting information is now:

- The accrual deferral days at the portfolio level is 10 days (same as before),

- The accrual cycle is 10, 20 and 30 (same as before),

- The ending day of the last End of Period Cycle Accrual is 31,

- The current date is the 20th of the month.

The starting day of the End of Period Cycle Accrual is the ending day of the last End of Period Cycle Accrual plus one, adjusted by 31 if the resulting value is greater than 31:

STARTING DAY = 31 + 1 = 32 - 31 = 1

The ending day of the End of Period Cycle Accrual is the current accrual cycle less the accrual deferral days at the portfolio level, adjusted by 31 if the resulting value is zero or negative:

ENDING DAY = 20 - 10 = 10

Therefore, leases with payment due days between the 1st and the 10th of the current month are accrued.

Accrual Reversal

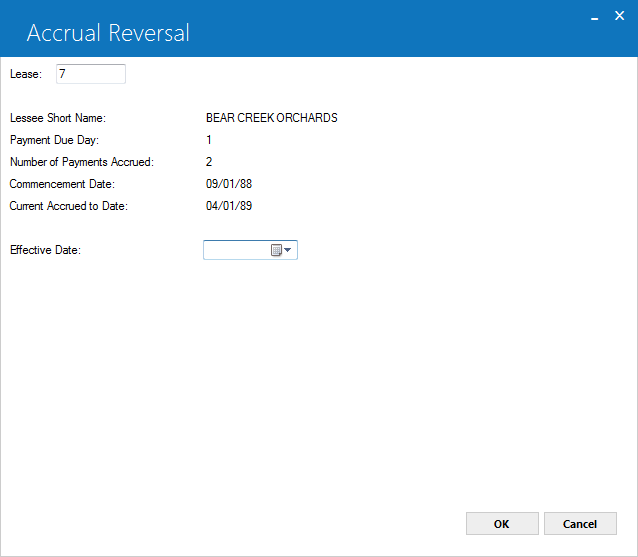

This screen is used to select the lease whose accrual is to be reversed.

This screen is used to enter the date back to which the accruals for the selected lease are to be reversed. Pertinent information about the lease is displayed.

All lease payments, use tax payments, vendor participation payments, and recurring charge payments made after the EFFECTIVE DATE must be reversed before accruals may be reversed for the lease. Use the Payment Reversal option of the Payments update [U0102] to reverse payments. The Accrual Reversal option does not reverse assessed late charges (and its associated sales tax, if the Sales Tax On Assessment module is purchased).

Assessed late charges must be waived using the Assessment Waiver option of the Assessment update [U0105].

This is the last screen of the Accrual Reversal option. When RETURN is pressed, the lease's accruals are reversed. If the accruals could not be reversed, a message is displayed indicating the problem, and no file updating is performed. If this occurs, correct the problem before attempting to reverse accruals again.

For example, if a payment due after the effective date is partially paid, a message indicating this is shown on the screen. Reverse the partial payment through the Payment Reversal option of the Payments update [U0102]. Then re-enter this update and try to reverse accruals again.

- LESSEE

SHORT NAME

The short name of the lessee is displayed.

- PAYMENT

DUE DAY

The payment due day of the lease is displayed.

- NUMBER

OF PAYMENTS ACCRUED

The current number of payments accrued for the lease is displayed.

- COMMENCEMENT DATE

The commencement date of the lease is displayed in MM/DD/YY or DD/MM/ YY format, depending on the Date Format Preference field in Security [U0706].

- CURRENT

ACCRUED TO DATE

The date to which the lease payments are currently accrued is displayed in MM/ DD/YY or DD/MM/YY format, depending on the Date Format Preference field in Security [U0706].

- EFFECTIVE

DATE

Enter the date in MM/DD/YY or DD/MM/YY format, depending on the Date Format Preference field in Security [U0706] to which the accruals for the lease are to be reversed. The EFFECTIVE DATE must be before the CURRENT ACCRUED TO DATE and on or after the COMMENCEMENT DATE. Also, the EFFECTIVE DATE must be a payment due date.For example, if lease payments are due monthly on the tenth of the month, the EFFECTIVE DATE must also be on the tenth of the month. If the lease payments are due quarterly (in January, April, July, and October) on the tenth of the month, the EFFECTIVE DATE must be either 1/10 or 10/01, 4/10 or 10/04, 7/10 or 10/07, or 10/10. It may not be 2/10 or 10/02, 3/10 or 10/03, etc.

General Ledger

Following are the sample general ledger entry used to reverse the dealer reserve amortization of a pre-computed lease:

| General Ledger Account | Amount |

| DR IDC7 - UNAMORT D/L DEALER RESERVE | Amount - ACC REV NORAML |

| CR IDC7 - AMOR D/L DEALER RESERVE |

Following are the sample general ledger entry used to reverse the dealer reserve amortization of an operating lease:

| General Ledger Account | Amount |

| DR IDC7 - UNAMORT O/L DEALER RESERVE | Amount - ACC REV NORAML |

| CR IDC7 - AMOR O/L DEALER RESERVE |

Following are the sample general ledger entry used to reverse the dealer reserve amortization of an interest-bearing loan:

| General Ledger Account | Amount |

| DR IDC7 - UNAMORT DEALER RESERVE | Amount - ACC REV NORAML |

| CR IDC7 - AMOR DEALER RESERVE |

Following are the sample general ledger entry used to reverse the accrual for a suspended pre-computed lease:

| General Ledger Account | Amount |

| DR IDC7 - UNAMORT D/L DEALER RESERVE | Amount - ACC REV NORAML |

| CR IDC7 - D/L SUSP DEALER BONUS |

Following are the sample general ledger entry used to reverse the accrual for a suspended operating lease:

| General Ledger Account | Amount |

| DR IDC7 - UNAMORT O/L DEALER RESERVE | Amount - ACC REV NORAML |

| CR IDC7 -O/L SUSP DEALER RESERVE |

Following are the sample general ledger entry used to reverse the accrual for a suspended interest-bearing loan:

| General Ledger Account | Amount |

| DR IDC7 - UNAMORT DEALER RESERVE | Amount - ACC REV NORAML |

| CR IDC7 -SUSP DEALER RESERVE |

Enhanced IDCs

Following are the general ledger transactions of additional IDC fields (IDC8–IDC9 and IDCA–IDCH) for accrual reversal:

For a precomputed type lease:

| Debit | Credit | ||

| 523 | IDC8–UNAMORT D/L RESERVES | 624 | IDC8 AMORTIZATION |

| 527 | ALT:IDC8–UNAMORT RESERVES | 654 | IDC8 – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 531 | IDC9–UNAMORT D/L RESERVES | 625 | IDC9 AMORTIZATION |

| 535 | ALT:IDC9–UNAMORT RESERVES | 655 | IDC9 – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 539 | IDCA–UNAMORT D/L RESERVES | 626 | IDCA AMORTIZATION |

| 543 | ALT:IDCA–UNAMORT RESERVES | 656 | IDCA – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 547 | IDCB–UNAMORT D/L RESERVES | 627 | IDCB AMORTIZATION |

| 551 | ALT:IDCB–UNAMORT RESERVES | 657 | IDCB – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 555 | IDCC–UNAMORT D/L RESERVES | 628 | IDCC AMORTIZATION |

| 559 | ALT:IDCC–UNAMORT RESERVES | 658 | IDCC – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 563 | IDCD–UNAMORT D/L RESERVES | 629 | IDCD AMORTIZATION |

| 567 | ALT:IDCD–UNAMORT RESERVES | 659 | IDCD – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 571 | IDCE–UNAMORT D/L RESERVES | 630 | IDCE AMORTIZATION |

| 575 | ALT:IDCE–UNAMORT RESERVES | 660 | IDCE – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 579 | IDCF–UNAMORT D/L RESERVES | 631 | IDCF AMORTIZATION |

| 583 | ALT:IDCF–UNAMORT RESERVES | 661 | IDCF – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 587 | IDCG–UNAMORT D/L RESERVES | 632 | IDCG AMORTIZATION |

| 591 | ALT:IDCG–UNAMORT RESERVES | 662 | IDCG – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 595 | IDCH–UNAMORT D/L RESERVES | 633 | IDCH AMORTIZATION |

| 599 | ALT:IDCH–UNAMORT RESERVES | 663 | IDCH – ALT: LEASE INCOME ADJUSTMENT |

For a suspended precomputed type lease:

| Debit | Credit | ||

| 523 | IDC8–UNAMORT D/L RESERVES | 634 | IDC8 – SUSPENDED AMORTIZATION |

| 531 | IDC9–UNAMORT D/L RESERVES | 635 | IDC9 – SUSPENDED AMORTIZATION |

| 539 | IDCA–UNAMORT D/L RESERVES | 636 | IDCA – SUSPENDED AMORTIZATION |

| 547 | IDCB–UNAMORT D/L RESERVES | 637 | IDCB – SUSPENDED AMORTIZATION |

| 555 | IDCC–UNAMORT D/L RESERVES | 638 | IDCC – SUSPENDED AMORTIZATION |

| 563 | IDCD–UNAMORT D/L RESERVES | 639 | IDCD – SUSPENDED AMORTIZATION |

| 571 | IDCE–UNAMORT D/L RESERVES | 640 | IDCE – SUSPENDED AMORTIZATION |

| 579 | IDCF–UNAMORT D/L RESERVES | 641 | IDCF – SUSPENDED AMORTIZATION |

| 587 | IDCG–UNAMORT D/L RESERVES | 642 | IDCG – SUSPENDED AMORTIZATION |

| 595 | IDCH–UNAMORT D/L RESERVES | 643 | IDCH – SUSPENDED AMORTIZATION |

For an operating type lease:

| Debit | Credit | ||

| 525 | IDC8–UNAMORT D/L–O/L RESERVES | 624 | IDC8 AMORTIZATION |

| 527 | ALT:IDC8–UNAMORT RESERVES | 654 | IDC8 – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 533 | IDC9–UNAMORT D/L–O/L RESERVES | 625 | IDC9 AMORTIZATION |

| 535 | ALT:IDC9–UNAMORT RESERVES | 655 | IDC9 – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 541 | IDCA–UNAMORT D/L–O/L RESERVES | 626 | IDCA AMORTIZATION |

| 543 | ALT:IDCA–UNAMORT RESERVES | 656 | IDCA – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 549 | IDCB–UNAMORT D/L–O/L RESERVES | 627 | IDCB AMORTIZATION |

| 551 | ALT:IDCB–UNAMORT RESERVES | 657 | IDCB – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 557 | IDCC–UNAMORT D/L–O/L RESERVES | 628 | IDCC AMORTIZATION |

| 559 | ALT:IDCC–UNAMORT RESERVES | 658 | IDCC – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 565 | IDCD–UNAMORT D/L–O/L RESERVES | 629 | IDCD AMORTIZATION |

| 567 | ALT:IDCD–UNAMORT RESERVES | 659 | IDCD – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 573 | IDCE–UNAMORT D/L–O/L RESERVES | 630 | IDCE AMORTIZATION |

| 575 | ALT:IDCE–UNAMORT RESERVES | 660 | IDCE – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 581 | IDCF–UNAMORT D/L–O/L RESERVES | 631 | IDCF AMORTIZATION |

| 583 | ALT:IDCF–UNAMORT RESERVES | 661 | IDCF – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 589 | IDCG–UNAMORT D/L–O/L RESERVES | 632 | IDCG AMORTIZATION |

| 591 | ALT:IDCG–UNAMORT RESERVES | 662 | IDCG – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 597 | IDCH–UNAMORT D/L–O/L RESERVES | 633 | IDCH AMORTIZATION |

| 599 | ALT:IDCH–UNAMORT RESERVES | 663 | IDCH – ALT: LEASE INCOME ADJUSTMENT |

For a suspended operating type lease:

| Debit | Credit | ||

| 525 | IDC8–UNAMORT D/L–O/L RESERVES | 634 | IDC8 – SUSPENDED AMORTIZATION |

| 533 | IDC9–UNAMORT D/L–O/L RESERVES | 635 | IDC9 – SUSPENDED AMORTIZATION |

| 541 | IDCA–UNAMORT D/L–O/L RESERVES | 636 | IDCA – SUSPENDED AMORTIZATION |

| 549 | IDCB–UNAMORT D/L–O/L RESERVES | 637 | IDCB – SUSPENDED AMORTIZATION |

| 557 | IDCC–UNAMORT D/L–O/L RESERVES | 638 | IDCC – SUSPENDED AMORTIZATION |

| 565 | IDCD–UNAMORT D/L–O/L RESERVES | 639 | IDCD – SUSPENDED AMORTIZATION |

| 573 | IDCE–UNAMORT D/L–O/L RESERVES | 640 | IDCE – SUSPENDED AMORTIZATION |

| 581 | IDCF–UNAMORT D/L–O/L RESERVES | 641 | IDCF – SUSPENDED AMORTIZATION |

| 589 | IDCG–UNAMORT D/L–O/L RESERVES | 642 | IDCG – SUSPENDED AMORTIZATION |

| 597 | IDCH–UNAMORT D/L–O/L RESERVES | 623 | IDCH– SUSPENDED AMORTIZATION |

For an interest–bearing loan:

| Debit | Credit | ||

| 521 | IDC8–UNAMORTIZED RESERVES | 604 | IDC8 – FASB91 INCOME ADJUSTMENT |

| 527 | ALT:IDC8–UNAMORT RESERVES | 654 | IDC8 – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 529 | IDC9–UNAMORTIZED RESERVES | 605 | IDC9 – FASB91 INCOME ADJUSTMENT |

| 535 | ALT:IDC9–UNAMORT RESERVES | 655 | IDC9 – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 537 | IDCA–UNAMORTIZED RESERVES | 606 | IDCA – FASB91 INCOME ADJUSTMENT |

| 543 | ALT:IDCA–UNAMORT RESERVES | 656 | IDCA – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 545 | IDCB–UNAMORTIZED RESERVES | 607 | IDCB – FASB91 INCOME ADJUSTMENT |

| 551 | ALT:IDCB–UNAMORT RESERVES | 657 | IDCB – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 553 | IDCC–UNAMORTIZED RESERVES | 608 | IDCC – FASB91 INCOME ADJUSTMENT |

| 559 | ALT:IDCC–UNAMORT RESERVES | 658 | IDCC – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 561 | IDCD–UNAMORTIZED RESERVES | 609 | IDCD – FASB91 INCOME ADJUSTMENT |

| 567 | ALT:IDCD–UNAMORT RESERVES | 659 | IDCD – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 569 | IDCE–UNAMORTIZED RESERVES | 610 | IDCE – FASB91 INCOME ADJUSTMENT |

| 575 | ALT:IDCE–UNAMORT RESERVES | 660 | IDCE – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 577 | IDCF–UNAMORTIZED RESERVES | 611 | IDCF – FASB91 INCOME ADJUSTMENT |

| 583 | ALT:IDCF–UNAMORT RESERVES | 661 | IDCF – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 585 | IDCG–UNAMORTIZED RESERVES | 612 | IDCG – FASB91 INCOME ADJUSTMENT |

| 591 | ALT:IDCG–UNAMORT RESERVES | 662 | IDCG – ALT: LEASE INCOME ADJUSTMENT |

| Debit | Credit | ||

| 593 | IDCH–UNAMORTIZED RESERVES | 613 | IDCH – FASB91 INCOME ADJUSTMENT |

| 5599 | ALT:IDCH–UNAMORT RESERVES | 663 | IDCH – ALT: LEASE INCOME ADJUSTMENT |

For a suspended interest–bearing loan:

| Debit | Credit | ||

| 521 | IDC8–UNAMORTIZED RESERVES | 614 | IDC8 – SUSP FASB91 INCOME ADJUSTMENT |

| 529 | IDC9–UNAMORTIZED RESERVES | 615 | IDC9 – SUSP FASB91 INCOME ADJUSTMENT |

| 537 | IDCA–UNAMORTIZED RESERVES | 616 | IDCA – SUSP FASB91 INCOME ADJUSTMENT |

| 545 | IDCB–UNAMORTIZED RESERVES | 617 | IDCB – SUSP FASB91 INCOME ADJUSTMENT |

| 553 | IDCC–UNAMORTIZED RESERVES | 618 | IDCC – SUSP FASB91 INCOME ADJUSTMENT |

| 561 | IDCD–UNAMORTIZED RESERVES | 619 | IDCD – SUSP FASB91 INCOME ADJUSTMENT |

| 569 | IDCE–UNAMORTIZED RESERVES | 620 | IDCE – SUSP FASB91 INCOME ADJUSTMENT |

| 577 | IDCF–UNAMORTIZED RESERVES | 621 | IDCF – SUSP FASB91 INCOME ADJUSTMENT |

| 585 | IDCG–UNAMORTIZED RESERVES | 622 | IDCG – SUSP FASB91 INCOME ADJUSTMENT |

| 593 | IDCH–UNAMORTIZED RESERVES | 623 | IDCH - SUSP FASB91 INCOME ADJUSTMENT |

U0301 Accrual Reversal produces the following general ledger transaction for the amount of IDC ASC 842 if the IDC ASC 842 accounting method (I/A/B) is set to 'A' - AMOR or 'B' - AMR2.

When lease is at Active status:

| Debit | Credit | ||

| 666 | UNAMORTIZED IDC COST - ASC 842 | 669 | IDC AMORTIZATION - ASC 842 |

When lease status is suspended:

| Debit | Credit | ||

| 666 | UNAMORTIZED IDC COST - ASC 842 | 667 | SUSPENDED IDC ACCRUED - ASC 842 |

Following are the general ledger transactions for the amount is IDC ASC 842 accrual reversal when Prorate Inc. IDC/IDR, Depr field is set to 'Y' from U0212 Portfolio → Miscellaneous Customizations.

When lease is at Active status:

| Debit | Credit | ||

| 666 | UNAMORTIZED IDC COST – ASC 842 | 670 | DEFERRED IDC AMORTIZATION – ASC 842 |

| 670 | DEFERRED IDC AMORTIZATION – ASC 842 | 669 | IDC AMORTIZATION – ASC 842 |

When lease status is suspended:

| Debit | Credit | ||

| 670 | DEFERRED IDC AMORTIZATION – ASC 842 | 669 | IDC AMORTIZATION – ASC 842 |

| 666 | UNAMORTIZED IDC COST – ASC 842 | 671 | DEFERRED SUSP IDC ACCRUED – ASC 842 |

| 671 | DEFERRED SUSP IDC ACCRUED – ASC 842 | 667 | SUSPENDED IDC ACCRUED – ASC 842 |

AOPM/ROPM Accrual Method

Following are the general ledger transactions for leases using *OPM accrual method:

| Debit | Credit | ||

| 82 | OPERATING LEASE INCOME | 60 | DEFERRED OPER LEASE REVENUE |

| 60 | DEFERRED OPER LEASE REVENUE | 3 | LEASE PAYMENTS RECEIVABLE |

| 82 | OPERATING LEASE INCOME | 60 | DEFERRED OPER LEASE REVENUE |

If the lease status is suspended:

| Debit | Credit | ||

| 103 | SUSPENDED INCOME ACCRUED | 60 | DEFERRED OPER LEASE REVENUE |

| 60 | DEFERRED OPER LEASE REVENUE | 40 | SUSPENDEDE RECEIVABLE (INCOME) |

If there was a last accrual transaction to clear the remaining balance in "Deferred Oper Lease Revenue" general ledger account, the following accrual reversal general ledger transaction will be done to reverse that:

| Debit | Credit | ||

| 82 | OPERATING LEASE INCOME | 60 | DEFERRED OPER LEASE REVENUE |

If the lease status is suspended:

| Debit | Credit | ||

| 103 | SUSPENDED INCOME ACCRUED | 60 | DEFERRED OPER LEASE REVENUE |

ARES/RRES Accrual Method

Following are the general ledger transactions for leases using *RES accrual method:

| Debit | Credit | ||

| 5 | LEASE INCOME RECEIVABLE | 3 | LEASE PAYMENTS RECEIVABLE |

| 284 | DEFERRED LESSOR INCOME - PRE | 5 | LEASE INCOME RECEIVABLE |

| 80 | LESSOR INCOME - PRECOMPUTED | 5 | LEASE INCOME RECEIVABLE |

If the lease status is suspended:

| Debit | Credit | ||

| 42 | SUSPENDED INCOME RECV (UNBILLED) | 40 | SUSPENDED RECEIVABLE (INCOME) |

| 103 | SUSPENDED INCOME ACCRUED | 4 | SUSPENDED INCOME RECV (UNBILLED) |

| 286 | DEFERRED SUSP INCOME ACCRUED | 42 | SUSPENDED INCOME RECV (UNBILLED) |

| 80 | LESSOR INCOME - PRECOMPUTED | 284 | DEFERRED LESSOR INCOME - PRE |

If there was a last accrual transaction to clear the remaining balance in the "Deferred Lessor Income - Pre" general ledger account, the following accrual reversal general ledger transaction will be done to reverse that:

| Debit | Credit | ||

| 80 | LESSOR INCOME - PRECOMPUTED | 284 | DEFERRED LESSOR INCOME - PRE |

If the lease status is suspended:

| Debit | Credit | ||

| 103 | SUSPENDED INCOME ACCRUED | 286 | DEFERRED SUSP INCOME ACCRUED |

For Vertex O users only: To process accrual reversal LeasePak checks that whether lease invoice is a Vertex O invoice or not. LeasePak reverse accruals on an invoice that was previously accrued by Vertex O interface tax calculations, and then the reversal process updates RVP database records with amount zero for the accrued tax and payment amounts. At the same time, LeasePak writes accrual reversal records to RVX table with a negative amount where the lease was originally accrued.

LeasePak Documentation Suite

©

by NetSol Technologies Inc. All rights reserved.